How to Fix Your Credit & Qualify for a Conventional Mortgage

Updated on April 21, 2025

There are many factors that lenders consider when approving mortgage applicants, but credit is the most notorious. Even if you have little to no debt and a high monthly income, a low credit score can really hurt your chances of qualifying for a conventional home loan.

It’s never too late to start repairing your credit so that you can qualify for the loan you want – read on to learn the fastest and most effective ways to raise your score.

Get a Conventional Mortgage by Raising Your Credit Score

While it’s possible to get a non-conventional mortgage loan with poor credit, these types of loans are not for everyone, at least not in the long run. For example, FHA loans are one of the most popular types of bad credit loans because they have very low down payment and credit score requirements. However, they also come with major disadvantages, including:

- Loan limits

- Mortgage insurance premiums that last the entire life of the loan

- Buying restrictions (property must meet certain standards)

- Higher interest rates

Conventional mortgage loans are less restrictive overall, and if your credit score is high enough, they cost less per month, too.

What credit score do I need for a conventional loan?

While there is no magic number that will guarantee you a loan, you will typically need a credit score of 620 or higher to qualify for a conventional mortgage loan. The higher your score, the lower your down payment, interest rate, and monthly payments will be. You can check your credit score at any time through your banking app or on a free website like Credit Karma.

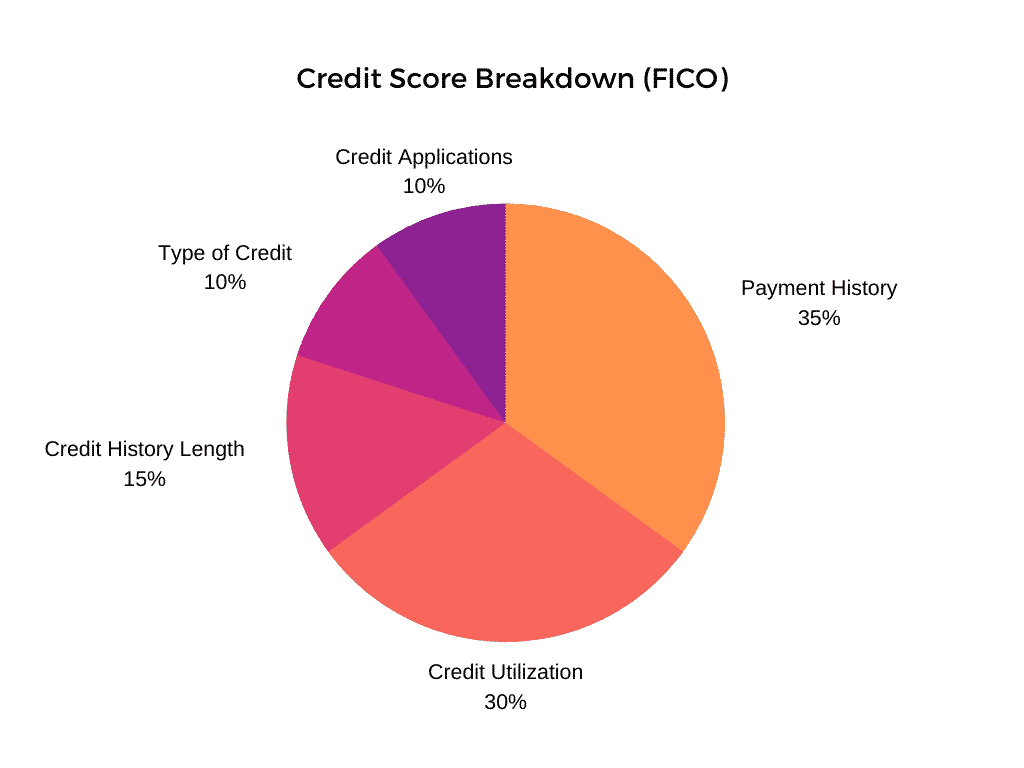

Credit Score Breakdown

You always pay your bills on time, so why is your credit score still holding you back from getting the mortgage loan you want?

While it’s important to stay on top of your monthly credit card bills, your payment history isn’t the only thing that affects your FICO credit score. FICO breaks your score down into five unique factors. You may be surprised to see that your payment history only contributes to 35% of your overall score.

Understanding the factors that affect your credit score will help you to make better decisions about the accounts you open and the way you spend. Here’s a closer look at the five categories and what they mean:

1. Payment history (35%)

Your payment history includes revolving credit (credit card payments) and installment credit (mortgages and car loans). Installment credit takes greater priority over revolving credit, which is part of the reason why homeowners tend to have better credit profiles than non-homeowners.

2. Credit utilization (30%)

Credit utilization refers to the percentage of your credit limit you use each month. If you’re regularly reaching of exceeding that limit, FICO’s credit formula will see you as a potential risk to lenders and lower your score accordingly. To avoid this penalty, it’s a good idea to keep your credit card balances low.

3. Credit history length (15%)

The length of time your credit accounts have been open is another major factor FICO considers. In many cases, you won’t even be given a score until your first account is more than 6 months old. Account age isn’t enough on its own – credit formulas also consider the amount of time since your last transaction.

4. Credit mix (10%)

FICO also considers your credit mix, or how many different types of credit you have. For example, a good credit mix might include monthly credit card payments, a mortgage loan, and an auto loan.

Your credit mix only contributes to a small portion of your credit score, so don’t worry if your account portfolio isn’t very diverse yet.

5. New credit applications (10%)

The last factor that FICO considers is the number of credit cards and loans you’ve applied for. Opening too many new accounts in a short amount of time can hurt your credit score, as can applying for credit you don’t qualify for.

What’s the Best Way to Raise Your Credit Score?

Establishing or rebuilding your credit is not something that happens overnight, but some methods are more effective than others.

Based on the five scoring factors above, it would make sense to focus on the largest category – payment history. As we mentioned before, credit scoring formulas place more importance on installment loans like mortgages and auto loans. For this reason, taking out an installment loan is one of the most effective ways to build your credit.

Using a Non-Traditional Mortgage Loan to Build Credit

If you’re not able to qualify for a conventional home loan right now, taking out a non-traditional loan and paying it on time can help your credit in a big way. In addition to improving your credit history, you’ll also be diversifying your credit mix, targeting two key factors that make up 45% of your overall score.

There are many different types of non-traditional home loans that can be used to build credit. For example, B/C Loans are often temporarily issued until the applicant can restore credit and qualify for a conventional mortgage loan.

Applicants for these types of loans typically have very poor credit, no credit, or have filed for bankruptcy in the past, putting a conventional mortgage loan far out of reach. If you’re only a few points shy of a qualifying credit score, there are other, less committal ways you can raise your score in a shorter period of time. These include paying off any past-due accounts and reducing the amount of your credit limit you use each month.

Talk to a Local Mortgage Professional

Improving your credit score takes time and consistency, but it’s never too late to start. If your goal is to be approved for a conventional home loan, a mortgage professional can help you take the right steps to get there.

Contact Associates Home Loan of Florida, Inc., to learn more about non-traditional mortgage loans and how they can help you establish a positive borrowing history.

Recent Posts

Your Guide to FHA Loan Limits in Florida (2026)

County Limits, Maximum Loan Amounts, and What Buyers Should Know Each year, the Department of Housing and Urban Development updates Federal Housing Administration (FHA) loan limits based on changes in median home prices across theRead More

What Does Escrow Mean?

A Guide to Escrow For Florida Homebuyers Escrow in real estate typically refers to money or documents held by a neutral third party to protect both the buyer and the seller during a transaction. InRead More

How to Sell Mortgage Notes in Florida

Turn Future Payments Into a Lump Sum If you want to sell a mortgage note, you’re likely looking to convert future mortgage payments into a lump sum of cash today. Selling a mortgage note allowsRead More